Orange County Experiencing Low Supply vs. Low Demand

August 30, 2022

SHARE

Even with ultra-low demand, the Orange County housing market lines up in favor of sellers due to the persistent lack of supply.

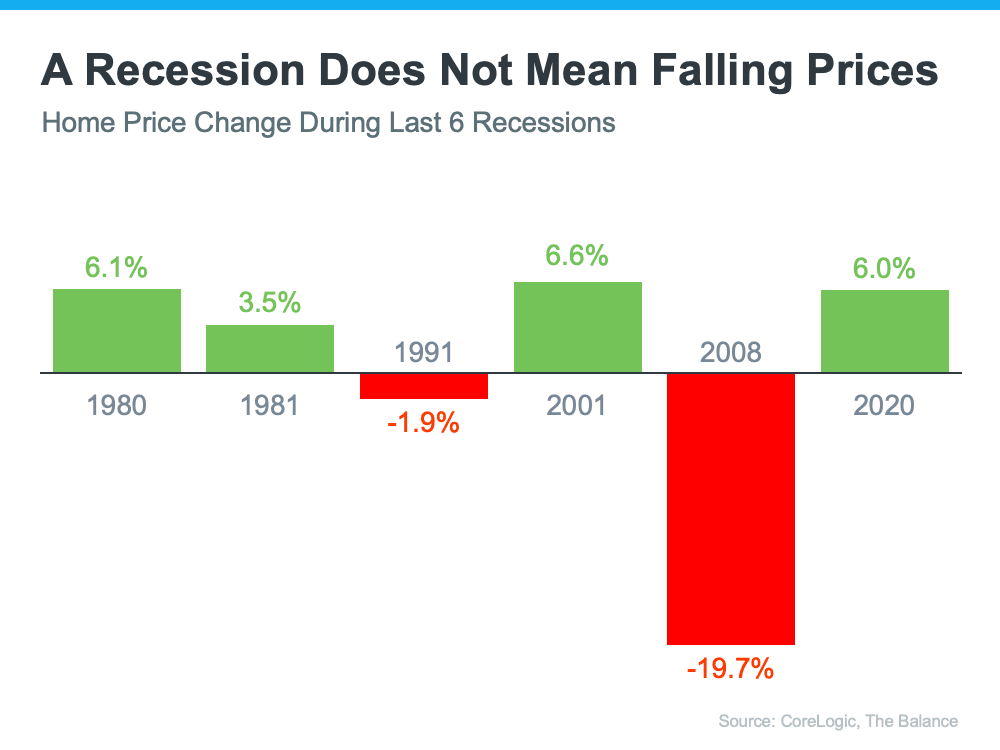

In the past week there has been a lot of noise about a “housing recession.” It was revealed that closed sales dropped in Laguna Niguel, Dana Point, Laguna Beach and Newport Beach in July. In Southern California, sales were off by 37% compared to 2021. As a result, proclamations from experts across the nation exclaimed that the housing market is officially in a recession. Unfortunately, way too many people will jump to the conclusion that values are going to plummet like they did during the Great Recession. The recession that experts are alluding to is a major drop in sales, fewer purchase and refinance loans, and an overall limited number of transactions for all those involved in the real estate industry. Yet, a recession does not mean that housing is in crisis and that values will plummet. Only two of the last six recessions prompted a drop in home values, the Savings and Loan Scandal of 1991 and the Great Recession, both instigated by the missteps of the housing industry. The other four recessions resulted in an appreciating housing stock.

Every recession is different. During the Great Recession unemployment skyrocketed and housing was a huge “house of cards” built on years of subprime loans, pick-a-payment plans, teaser rate adjustable mortgages, and fraudulent lending practices. It was not a shock that housing values sank. This “recession” will be entirely different. Thus far in 2022, the Orange County housing market has slowed from an Expected Market Time (the time between hammering in the FOR-SALE sign to opening escrow) of 19 days in early March to 65 days today, yet the slowing has stopped. In fact, the market time has dropped by 7 days since climbing to 72 days a month ago. To understand why housing has shifted but is not on the verge of collapse, look no further than to good old-fashioned supply and demand.

On the demand side of the equation (a snapshot of the number of new escrows over the prior month), buyer activity has been muted all year. A premature peak was reached at the end of March with 2,286 pending sales, down 28% from last year’s peak of 3,162 pendings. Compared to the 3-year average peak prior to COVID (2017 to 2019) of 2,816, this year

was 19% less. Today, demand sits at 1,849, slightly higher than where it stood a month ago at 1,693. Even with the recent rise, today’s reading is the lowest level for this time of year since 2007, the start of the Great Recession. The current demand level is typically reserved for the slowest time of the year for real estate, January, with a 3-year average pending sales(2017 to 2019) of 1,551 pending sales, and December, 3-year average of 1,637. The August 3-year average is 2,506 pending sales, 36% higher than today.

Today’s demand levels are significantly muted due to mortgage rates rising from 3.25% at the start of the year to 5.72% where they stand today, according to Mortgage News Daily. The buyer pool has been impacted and reduced by the massive drop in affordability that accompanies such a steep rise in rates.

Yet, muted demand is being matched up against a severely muted supply of available homes to purchase. The inventory dropped to a record low level on January 1st of this year with only 954 homes. As a result of diminished demand, the inventory was able to rise to 4,069 homes at the start of August, an increase of 327%. Yet, the inventory reached what appears to be a peak a couple of weeks ago. It dropped by 39 homes in the past two weeks and sits at 4,030 homes today. The issue is that the inventory is still far below normal for this time of year. While it may be higher than last year’s 2,528 home mark in mid-August, it is still the second lowest reading since tracking began in 2004. The 3-year average August inventory (2017 to 2019) was 6,646 homes, 65% higher than today.

.

With muted demand, how has the Orange County inventory already reached a peak? The first factor is that demand has reached a cruising altitude, stabilized after slowly dropping since the end of March. The second factor, and more importantly, there are fewer homeowners opting to sell. Fewer homes coming on the market impacts the ability for homes to accumulate on the market and allow the inventory to grow faster. From January to July of this year there have been 17% fewer FOR SALE signs compared to the 3-year average prior to COVID (2017 to 2019), a shocking 4,373 missing signs. In all of 2020, there were 1,795 missing signs, and there were 2,311 in all of 2021. This is a new trend that started in January as mortgage rates were rising.

Homeowners are not moving because they simply do not want to sell as they are locked into an incredibly low fixed mortgage rate. 72% of all homeowners have a mortgage rate at 4% or lower. 55% have a rate at 3.5% or lower. 34% have a rate at 3% or lower. If a homeowner sells and opts to purchase a replacement property, they are going to be paying a much higher rate and, most likely, much higher property taxes. Thus, homeowners are staying put. They may not be in love with their home, but they certainly are in love with their loan.

Another factor that has contributed to the diminished supply is that many sellers who have been unable to sell have decided to pull their homes off the market. For the first couple of weeks of August, the number of homes that have come off the market without success is up 127% compared to the same time last year.

The giant drop in demand is being matched up against an extremely anemic supply of available homes. There are fewer buyers participating today, just as there are fewer homeowners participating. This will continue until mortgage rates shift either higher or lower. Until then, the battle between supply and demand continues.

Active Listings

The current active inventory most likely peaked a couple of weeks ago.

The active listing inventory decreased by 39 homes, down 1%, and now sits at 4,030, its first drop since the end of March and the largest drop of the year. Now that the inventory is establishing a peak, it will continue to slowly descend from now until mid-November, just prior to Thanksgiving. From that point through New Year’s Eve, the inventory will plunge just as it does every single year. With the inventory falling for the remainder of the year, it paves the way for a very low start to 2023.

Last year, the inventory was at 2,528, 37% lower, or 1,502 fewer. The 3-year average prior to COVID (2017 to 2019) is 6,723, an extra 2,693 homes, or 67% more. There were a lot more choices back then.

Demand

Demand increased by 2% in the past couple of weeks.

Demand, a snapshot of the number of new escrows over the prior month, increased from 1,812 to 1,849 in the past couple of weeks, adding 37 pending sales, or up 2%, its highest level since the end of June. With the recent rises in mortgage rates from 5.05% on August 1st to 5.72% today, the 4-week rise in demand will most likely subside until rates shift lower. Mortgage rates have been a lot more volatile this month as the Federal Reserve is no longer purchasing Mortgage-Backed Securities and is now draining their balance sheets. That simply means that the secondary market is functioning on its own without the Federal Reserve propping it up like it was during 2020 through 2021. Without their help in stabilizing the mortgage market, rates have been jumping all over the place. The rate a buyer sees today may be completely different tomorrow. It behooves buyers to closely monitor rates with their mortgage consultant.

Last year, demand was at 2,594, 46% more than today, or an extra 845. The 3-year average prior to COVID (2017 to 2019) was at 2,574 pending sales, 39% more than today, or an extra 725.

With supply falling and demand rising, the Expected Market Time (the number of days to sell all Orange County listings at the current buying pace) decreased from 67 to 65 days in the past couple of weeks, the lowest level since the end of June. At 65 days, it remains a SlightSeller’s Market (60 to 90 days) where sellers get to call most of the shots, there are fewer multiple offers and home values are not appreciating as fast as they have been over the past couple of years. The market is no longer instant and properly pricing is crucial to find success. Last year the Expected Market Time was at 28 days, substantially faster than today. The 3-year average prior to COVID was at 79 days, also a Slight Seller’s Market and a touch slower than today.

Luxury End

The luxury housing market continued to improve over the last couple of weeks.

In the past couple of weeks, the luxury inventory of homes priced above $2 million decreased from 837 to 820 homes, down 17 homes, or 2%, and its first drop since February. Luxury demand increased by 8 pending sales, up 4%, and now sits at 209, its highest reading since June. With supply dropping and demand increasing, the overall Expected Market Time for luxury homes priced above $2 million decreased from 125 to 118 days, its best reading since June. Even with the improvement, for perspective, it was at 45 days back in February, an insanely HOT Seller’s Market for luxury. Wall Street’s volatility will continue to impact the upper end of Orange County’s housing market.

Year over year, luxury demand is down by 21 pending sales or 9%, and the active luxury listing inventory is up by 199 homes or 32%. The Expected Market Time last year was at 81 days, stronger than today.

For homes priced between $2 million and $4 million, the Expected Market Time in the past two weeks decreased from 99 to 98 days. For homes priced between $4 million and $8 million, the Expected Market Time decreased from 179 to 159 days. For homes priced above $8 million, the Expected Market Time decreased from 320 to 225 days. At 225 days, a seller would be looking at placing their home into escrow around April 2023.

Orange County Housing Summary

The active listing appears to have reached a peak a couple of weeks ago with a 39 home drop, or 1%, and now sits at 4,030 homes. In July, there were 19% fewer homes that came on the market compared to the 3-year average prior to COVID (2017 to 2019), 721 fewer. Last year, there were 2,528 homes on the market, 1,502 fewer homes, or 37% less. The 3-year average prior to COVID (2017 to 2019) was 6,723, or 67% more.

Demand, the number of pending sales over the prior month, increased by 37 pending sales in the past two weeks, up 2%, and now totals 1,849. It is still the lowest reading for mid-August since 2007. Last year, there were 2,694 pending sales, 46% more than today. The 3-year average prior to COVID (2017 to 2019) was 2,574, or 39% more.

With supply falling and demand rising, the Expected Market Time, the number of days to sell all Orange County listings at the current buying pace, decreased from 67 to 65 days in the past couple of weeks, a Slight Seller’s Market (between 60 and 90 days). It was at 28 days last year, much stronger than today.

For homes priced below $750,000, the market is a Hot Seller’s Market (less than 60 days) with an Expected Market Time of 47 days. This range represents 20% of the active inventory and 28% of demand.

For homes priced between $750,000 and $1 million, the Expected Market Time is 62 days, a Slight Seller’s Market. This range represents 25% of the active inventory and 26% of demand.

For homes priced between $1 million to $1.25 million, the Expected Market Time is 60 days, a Slight Seller’s Market. This range represents 12% of the active inventory and 14% of demand.

For homes priced between $1.25 million to $1.5 million, the Expected Market Time is 65 days, a Slight Seller’s Market. This range represents 11% of the active inventory and 11% of demand.

For homes priced between $1.5 million to $2 million, the Expected Market Time is 75 days, a Slight Seller’s Market (between 60 and 90 days). This range represents 11% of the active inventory and 10% of demand.

For homes priced between $2 million and $4 million, the Expected Market Time in the past two weeks decreased from 99 to 98 days. For homes priced between $4 million and $8 million, the Expected Market Time decreased from 179 to 159 days. For homes priced above $8 million, the Expected Market Time decreased from 320 to 225 days.

The luxury end, all homes above $2 million, accounts for 21% of the inventory and 12% of demand.

Distressed homes, both short sales and foreclosures combined, made up only 0.2% of all listings and 0.3% of demand. There are only 5 foreclosures and 2 short sales available to purchase today in all of Orange County, 7 total distressed home on the active market, unchanged from two weeks ago. Last year there were 12 total distressed homes on the market, similar to today.

There were 1,959 closed residential resales in July, 39% less than July 2021’s 3,205 closed sales. July marked a 17% decrease compared to June 2022. The sales to list price ratio was 100.7% for all of Orange County. Foreclosures accounted for 0.05% of all closed sales, and short sales accounted for 0.05%. That means that 99.9% of all sales were good ol’ fashioned sellers with equity.

Copyright 2022- Steven Thomas, Reports On Housing – All Rights Reserved. This report may not be reproduced in whole or part without express written permission by author.