Orange County Housing Report: A 2023 Forecast

HAPPY NEW YEAR!!! Now, what does that mean for Orange County real estate?

The 2023 Forecast: A subdued year for housing.

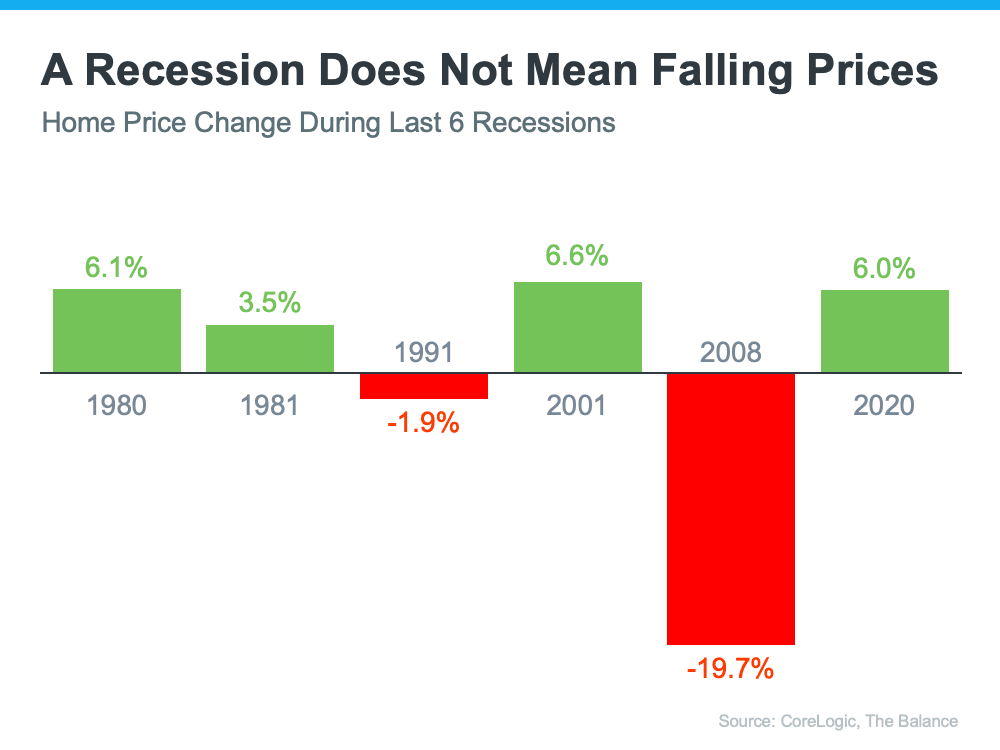

After two years of runaway home prices, the Federal Reserve stepped in to reverse engineer rampant inflation and has been utilizing the housing market as one of the main economic engines to achieve its objective. They increased the Federal Funds Rate from nearly 0% at the start of the year to 4.5% in December, its highest level since 2007 and its fastest rise in more than 40 years. Long-term mortgage rates responded rising from 3.25% at the start of the year to over 7.25% in October, more than doubling. They eased below 6.5% in December as inflation numbers began to improve for the second consecutive month. Yet, inflation remains elevated, up 7.1% year over year through November. It hit 9% in June. Core inflation, less the volatility of food and energy, is currently at 5.96%, after reaching 6.7% in September. The Federal Reserve’s core inflation goal is 2%, so they have a long way to go. The overall United States economy has remained resilient backed by a very strong labor market, sky-high job openings, low unemployment, and increasing consumer spending. Yet, the high-interest rate environment has been rocking the financial markets. The unrelenting Federal Reserve policies will eventually instigate an economic recession in 2023 that will most likely begin by mid-year. As a result, the local housing market is going to be subdued in 2023, especially in the first half of the year. Here is the forecast:

- Active Inventory – the year will begin with less than 2,500 homes, the second lowest start to a year since tracking began in 2004. Only the start of 2022 was lower, 62% less. Prior to COVID, the average start was 4,420, with 77% more available homes to purchase. The inventory crisis will continue. Expect the inventory to rise on the back of diminished demand, only to be hampered by the “Hunkering Down” effect where homeowners opt to stay in their homes due to their underlying low mortgage rates. More homes will enter the fray once mortgage rates drop below 5.5%, most likely sometime in mid-2023. Expect the active inventory to peak around August eclipsing 5,500 homes, well below the over 7,000 home peak average prior to COVID.

- Demand – due to the persistent high mortgage rate environment, buyer demand will continue to be muted. With less competition and pressure on affordability, buyers will be extremely cautious and unwilling to stretch above the asking price. They will be looking very carefully at price; so, expect home values to drop between 6.5 to 8.5% for the year. There is a strong potential for mortgage rates to dip below 5.5% by the summer due to the combination of a slowing economy and falling inflation. With lower rates, demand will strengthen along with affordability. The combination of lower rates and lower home prices will prompt this rise in pending sales activity.

- Housing Cycle - the housing market will follow a normal housing cycle. The strongest demand coupled with the highest levels of new sellers will occur during the Spring Market. This will be followed by slightly less demand and a continued new supply of homes in the Summer Market. From there, demand will drop further along with fewer homes entering the fray in the Autumn Market. Finally, all the distractions of the Holiday Market will be punctuated with the lowest demand of the year and few homeowners opting to sell.

- Closed Sales - the number of successful, closed sales will decrease by 6.5 to 8% compared to 2022, with around 22,900 (the lowest sales volume since 2007).

- Luxury Market – luxury housing will be sluggish and will continue to transition to normal, longer market times, often taking months to procure a sale. The Spring Market will be the strongest for luxury and will become a bit more sluggish and susceptible to Wall Street volatility during the second half of the year.

- Interest Rates – look for mortgage rates to start around 6.5% and slowly, but methodically drop as the economy slows, and inflation gradually eases. As the United States economy slips into a recession, expect rates to fall to below 5.5% and may even fall to below 5% by year’s end. If mortgage rates recede to these levels, housing will stabilize, and home values will stop their decline.

- Distressed Inventory – do not expect a wave of foreclosures. The number of active forbearances has dwindled to very low levels. Of the over 7.8 million forbearance exits, 91% are either performing monthly or paid off their loans. Only 1% are in active foreclosure, less than 100,000 across the United States, and the current delinquency rate is at its lowest level in decades. Expect slightly more distressed sales in 2023 as there are some homeowners who will be susceptible to an economic downturn. Nonetheless, the total numbers will be very low and undetectable in the broader housing market.

The bottom line: 2023 will continue where housing in 2022 left off, extremely sluggish. Housing is particularly interest rate sensitive, where even with anemic, low inventory levels, values will still drop due to severe affordability issues. Values will stop retreating only when mortgage rates drop below 5.5%, instigating more demand and more homeowners to stop “Hunkering Down” and list their homes at a more normal rate. The housing market is no longer insane, homes are for the most part not selling above their asking price, not selling immediately, not selling with multiple offers, and there is far less activity and buyer competition.